Answering Investor’s Most Pressing Questions

John P. Swift, CFA, CPA Chief Investment Officer

312-259-9595 or jswift@trustbenchmark.com

June 15, 2020

In our past several notes, “What Banking Stocks are Saying About Economic Recovery”, 5/18/20 and “We’ve Got High Hopes”, 6/1/20, we have been discussing that the stock market has been consciously blocking out the acute economic pain of the COVID-19 impact today in favor of a vision that revolves around a return to normalcy that is ushered in with fiscal and monetary policy support and accompanied by the arrival of an effective vaccine.

What is clear is that the fear and panic in late February and into March that was caused by the economic shutdown in response to the COVID-19 pandemic was replaced by confidence provided by the river of liquidity coming from the U.S. Federal Reserve and the welcome fiscal relief provided by Congress and the President. The rally off the March 23rd low occurred in the face of declining earnings estimates, which is another way of saying there was some major multiple expansion. Three months ago, the S&P 500 traded at 14.5x forward twelve-month earnings. Today, it trades at nearly 22x forward twelve-month earnings. It hit 23x only a few days ago, which is as high as it has been since the dot-com era.

Against that dichotomy or tremendous stock market performance juxtaposed against continually alarming economic data, I would like to address the most common questions investors are asking today such as:

1. How do we make sense of the disconnect between the disastrous economic data and near-record high US

stock indices? 2. Against the high relative market valuation, would it make sense to sell the rally? 3. Aren’t equity valuations too elevated to begin re-risking portfolios now? 4. Isn’t the massive monetary and fiscal liquidity infusion into our economy ultimately inflationary? 5. Has the much-anticipated rotation from growth stocks to value stocks finally commenced? 6. Several of the states that were in the process of reopening their economy have seen increased coronavirus cases. Should we be concerned about the prospects of reclosing major parts of our economy?

1. How do we make sense of the disconnect between the disastrous economic data and near-record high US stock indices?

Markets are forward-looking mechanisms. The near-40% decline in the S&P 500 Index from February 19th to March 23rd was the market pricing in the ruinous economic data being released during that time, and potentially more still yet to be released. As a result, lagging economic indicators, such as gross domestic product and the unemployment rate, will likely be of little future consequence to the market. Instead, markets are trading, and will likely continue to trade, not on whether conditions are good or bad, but rather on whether circumstances are getting better or worse.

There is little that is “good” about the current environment, but conditions have improved markedly since the March 23rd bottom. Fiscal and monetary policy have been effectively implemented on a global scale, the fears of the pandemic have receded with caseloads and hospitalizations down meaningfully in many of the hardest hit areas (Milan, New York for example), human mobility is picking up, and economic activity is noticeably rebounding.

Finally, there has been a noticeable spike in infections in some areas this past week which was one of the primary causes of the market’s increased volatility, but only time will tell if these new increased caseloads will continue or if we will see a continuation of the downward trajectory of new cases experienced over the past several weeks.

The Federal Reserve Chairman Powell also did not do the markets any favors this past week by talking down the economy in his press conference on Wednesday. Chairman Powell reminds me of a guy who steps in to save a struggling restaurant, only to turn around and write a scathing review of that restaurant’s food. Seriously, Chairman Powell needs to keep interest rates at zero, buy a bunch of risky debt, and quit being a market prognosticator.

2. The market is now priced for perfection. Wouldn’t it make sense to sell the rally?

If investors have learned anything over the past three months, it should be about the “loser’s game” of trying to time markets. Case in point, money market assets at the beginning of March were $3.6 trillion and currently stand at a record $4.8 trillion. The challenge of de-risking portfolios is knowing when to reenter the market. The 40% rally in the S&P 500 Index since March 23rd is proof of that. Waiting for exceptional economic data has historically been a mistake. Markets in the years following the global financial crisis, for example, had already staged a sizeable rally by the time that mortgage default rates peaked, household balance sheet deleveraging concluded, and weekly jobless claims returned to average.

It is true that there are still many challenges ahead and policymakers need to effectively bat four for four with regards to getting monetary policy, fiscal policy, re-opening policy, and trade policy right. A dreaded second wave of COVID-19 cases could be in the offing, potentially creating renewed volatility in markets. However, markets will likely be focusing attention on the long-term prospects of a very slow and prolonged recovery supported by massive policy support and a protracted period of low interest rates, all of which should ultimately be supportive of equity and credit markets. Being structurally short equity markets here is akin to betting against policymakers, human ingenuity, science, and medicine.

3. Aren’t equity valuations too elevated now?

Historically, valuations have been extremely poor timing tools, having little to no statistical impact on short- to intermediate-term returns. Equity multiples tend to rise in market recoveries as the market prices in a forthcoming

recovery in economic activity and earnings growth. Finally, stocks continued to trade cheap to most other asset classes, including US government-related securities and investment-grade corporate bonds.

4. Isn’t this all inflationary?

That is the idea. The demand destruction resulting from the COVID-19 outbreak and the subsequent shutting down of large segments of the economy have unleashed deflationary forces on the global economy. Deflation is the worst of all outcomes as consumers and investors put off consumption and investing expecting prices to fall more in the future while static debt loads become more unaffordable as currency value depreciates.

The US Federal Reserve, per its dual mandates of maintaining price stability and full employment, has responded aggressively to reflate the economy and asset prices. The Fed’s actions are proving successful (note the recent decline in the US dollar and the rise in commodity prices) but are unlikely to unleash massive inflationary pressures on the US economy. Structural forces against inflation, including an aging population globally and technological progress, remain and will now be compounded by a protracted period of elevated unemployment globally.

5. Has the much-anticipated rotation from growth stocks to value stocks finally commenced?

A more accurate assessment than a rotation would be a widening of the breadth of the market (currently more than 95% of the companies in the S&P 500 Index are trading above their 50-day moving average). Value stocks finally started to participate in recent weeks, even as growth stocks outperformed in the month of May.

For value to outperform growth, there needs to be a catalyst. Successful reopening of large segments of the economy and subsequent improvements in economic activity would likely be that catalyst. Sectors and industries such as financials, energy, hotels, and airlines would be likely beneficiaries. If instead we emerge from the pandemic in inconsistent and irregular intervals, then it is likely to be an environment that continues to favor true growth companies.

Our present portfolio construction strategy is to focus on companies with industry-leading positions, sound balance sheets, and secure dividends heavily weighted toward information technology, consumer discretionary and other growth sectors while also having significant weighting to more defensive sectors such as healthcare and consumer staples. This is our “two hulls in the water catamaran strategy” we highlighted in our recent “Market Outlook & Portfolio Strategy” note where we might give up a little upside if the economy has a “V”-shaped recovery, but we will be ready to provide stability in rough seas if the economic rebound does not go as planned.

6. Several of the states that were in the process of reopening their economy have seen increased coronavirus cases. Should we be concerned about the prospects of reclosing major parts of our economy?

The number of confirmed coronavirus cases continues to rise in U.S. states that were among the first and most aggressive to reopen, leading some local officials to reconsider reopening plans. In Oregon, Gov. Kate Brown announced a 7-day statewide pause on further reopening as health officials study the data and try to contain budding outbreaks.

In Arizona, however, Gov. Doug Ducey tried to reassure people that the rise in confirmed cases was expected and that the state’s hospitals have the capacity to handle a further surge.

It has been known for months that once we reopened our economy that we were going to see an uptick in COVID- 19 infections. This was known with absolute certainty. The fact that we are now experiencing increased infections in states that have been in the process of reopening should not be a surprise. However, the market has been trading as if it carries a zero tolerance for any uptick and is trading as if states will re-close major parts of our economy. This is an overreaction as far as we are concerned.

Underfunded Public Pension Debt & Municipal Bond Yields

The recent 2020 update on public pensions from the Center for Retirement Research at Boston College found that on balance municipal pension plans can endure and will maintain sufficient assets from which to pay benefits. However, some plans with extremely low funded ratios face an increased risk of exhausting their assets and the high cost of pay-as-you-go funding if they do.

In 2020, the average estimated funded ratio for the 20 worst-funded plans in their sample is 38.3%. If markets are slow to recover, their average funded ratio will drop to 32.2% in 2025. Six plans – Charleston (WV) Fire, Dallas Police and Fire, Chicago Municipal, Chicago Police, Chicago Teachers, and New Jersey Teachers – will end up with funded ratios of 25 percent or less. Given the low funded ratios, the question turns to the extent to which of these plans will be able to pay benefits.

The key metric on this is the ratio of assets to benefits. For the 20 worst-funded plans, the average ratio is projected to decline slightly from 5.9 in 2020 to 4.5 in 2025. That figure means that, in 2025, they will have on hand assets equal to less than five years of benefits. Chicago Municipal, Dallas Police and Fire, and New Jersey Teachers, which have severely negative cash flows, will see their asset-to-benefit ratios deteriorate even more dramatically – ending the period with assets equal to less than two years of benefit payments.

Reaching an actual depletion date can have a severe impact on a state’s finances because a sudden transition to a pay-as-you-go plan may result in costs that far exceed recent employer contributions. As an example, pay-as- you-go costs for both New Jersey Teachers and Chicago Municipal were more than 50 per cent higher than their contributions.

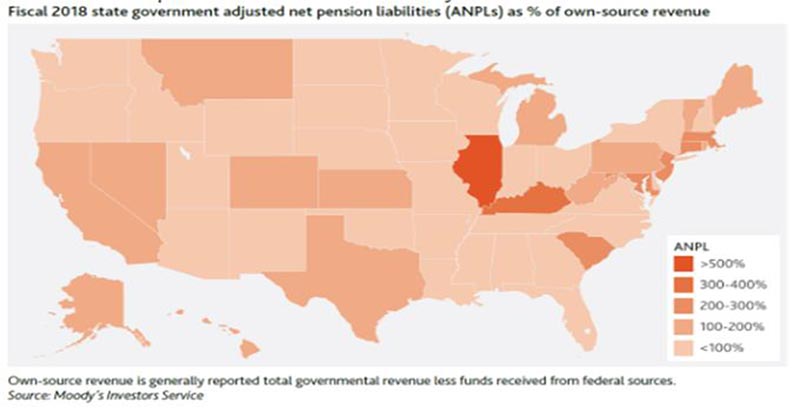

The graph below provides a scale of the state’s unfunded public pension liabilities as a percentage of state “own source” revenues. “Own source” state revenues are generally defined as total governmental revenues less the funds received from federal sources. As the graph indicates, the State of Illinois would need to allocate 100% of its “own source” state revenues towards funding its unfunded public pension debt for close to the next six years before it balanced the books on the retirement plan promises that it has made to its public employees. That is

close to six years without having any revenues to fund state services. It is obviously theoretical as the state would not shut down in this manner, but putting things into perspective this would mean that in addition to no more police and corrections for six years, you would lose all your elementary and secondary education, public welfare (which includes most Medicaid spending), higher education, health and hospitals, fire department, highways and roads.

Obviously, Illinois would never shut down for six years, but it does bring up an important point on whether Illinois municipal bond investors are being adequately compensated for the fiscal time bomb underpinning their bond purchases.

Catching Up

We look forward to catching up with each of you, and we will be reaching out to schedule a time to meet over the phone or by a Zoom video link. In the interim, if you would like to get something on the calendar, please send me a note with some dates and times.

Warm regards, John