Q2: 2019 Market Outlook

Market Update – 2Q19A

A lot can happen in three months, and the stock market is off to its best start since 1987. That start is a far cry from how 2018 finished, yet it’s a byproduct of why the stock market climbed more than 300% from its 2009 low and set a record high in September 2018.

In short, it’s a byproduct of market-friendly monetary polict.

So Good

When we wrote our “1Q18 Market Outlook” in late December 2018, the S&P 500 was in a tailspin, as market participants’ heads were spinning on an axis of concern that the Federal Reserve (“Fed”) was being too aggressive with its monetary policy and placing the U.S. economy on a crash course to recession.

On Christmas Eve the S&P 599 dropped 65 points, or 2.7%, to 2351.10, leaving it down 14.8% for the month of December alone.

At that time our 2019 prediction was as follows (1Q19 Market Outlook, 1/8/19) “What we believe coming out of 2019 is that long-term investment prospects are looking better than they did entering 2019, and we are forecasting a total return for the U.S. equity market in the mid-teens for 2019″. At the time, we were going against the popular opinion that the market was positioned for further losses.

However, since Christmas Eve, the S&P 500 has risen 21.4%. That move has been paced by the outperformance of the cyclical sectors, yet it has been underpinned by positive contributions from every sector.

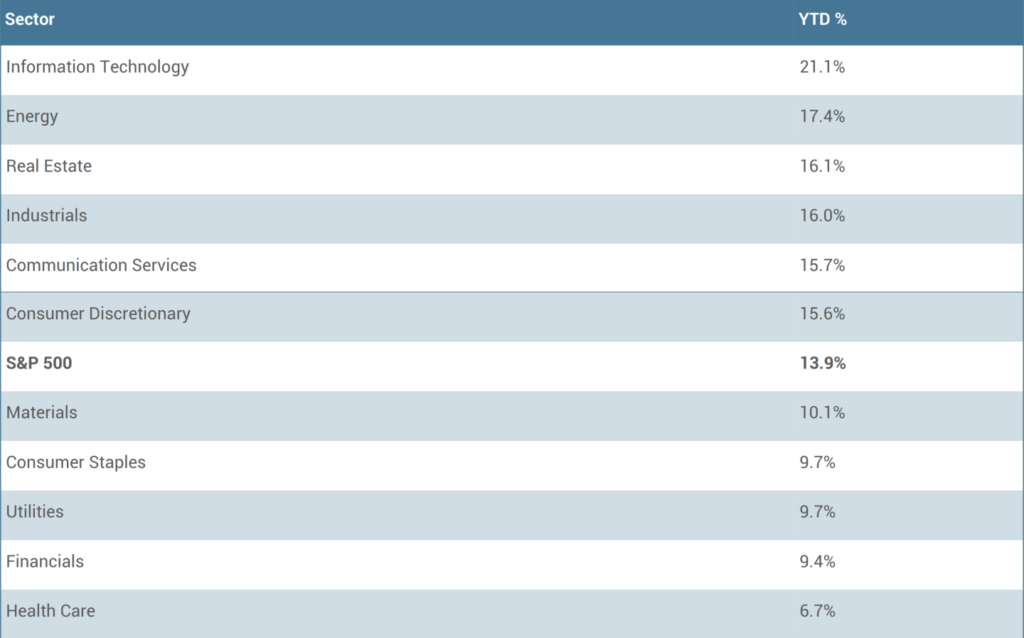

How good has it been? The health care sector is up 6.7%, and it is the worst-performing sector! The S&P 500, meanwhile, is up 13.9%.

What changed?

- The rebound started with a belief that the market had gotten oversold and was due for a bounce.

- There was a burgeoning sense that the stock market fallout in the fourth quarter would compel President Trump to strike a trade deal relatively soon with China.

- The employment report for December quieted recession concerns, as it featured a 312,000 increase in nonfarm payrolls and a 0.4% uptick in average hourly earnings.

The biggest change agent, though, has been the Fed.

Messaging Counts

The Fed changed its message on January 4 with an acknowledgment from Fed Chair Powell that the Fed is going to be patient before changing monetary policy. That was music to the ears of the stock market, which heard “we won’t be raising the fed funds rate anytime soon.”

Mr. Powell also asserted that the Fed would be open to making changes to the balance sheet runoff plan, which he said only weeks before was on auto pilot.

Flash forward to the March FOMC meeting, which culminated with a decision to leave the target range for the fed funds rate unchanged at 2.25% to 2.50%, produced an updated dot plot that showed a median estimate for no rate hikes in 2019 (down from two rate hikes at the time of the December 2018 meeting), and a clarification that the balance sheet runoff will be completed at the end of September 2019.

That dovish-minded message came just two weeks after the European Central Bank told the world its key interest rates are expected to remain unchanged at least through the end of 2019 (versus prior guidance for at least through the end of summer), which was joined with pledges out of China to use fiscal and monetary policy to support the economy, and no inclination on the part of the Bank of Japan or the Bank of England to raise their key rates anytime soon.

The world’s major central banks, then, have all said “easy does it” with their monetary policy, which in turn has made for some easy money so far in 2019 for equity investors.

The S&P 500 is up 13.9% year-to-date; China’s Shanghai Composite is up 24.4%; Japan’s Nikkei is up 8.0%; Germany’s DAX Index is up 9.4%; and the UK’s FTSE 100 is up 8.4%.

Those gains have all been logged in the face of slowing growth, falling earnings estimates, trade deal uncertainty, and a mess of a Brexit plan that remains unknown just a week in front of the UK’s scheduled March 29 divorce date from the EU.

Hope springs eternal for equity investors, though, when they don’t need to live in fear of central banks raising interest rates. The persistence of low rates is the pathway to better days ahead — or so it is believed.

Focused on 2019 Second Half

Interest rates that stay low buy some time to get economic growth and earnings estimate trends turned around. That thinking is at work today and it has manifested itself in the outperformance of the cyclical sectors.

Things may be challenging now, but they’ll be getting better in the back half of the year. That is the message of a stock market that has enjoyed multiple expansion at a time when it seems unjustified.

Currently, the S&P 500 trades at 16.6x forward twelve-month earnings. That is above its 5-yr and 10-yr averages of 16.4x and 14.7x, respectively, and up from 14.2x when we published our Market Outlook in December. The thrust of that view was that the discounted valuation provided an attractive entry point for long-term investors.

So, now that the forward twelve-month P/E multiple is above its short-term and long-term averages, what is the view today?

In brief, the investment view is less upbeat, yet it isn’t beaten up. We expect this market to show some fight still after picking itself off the fourth quarter mat.

What this Means to You

Market rates are lower than they were when the year began. That’s a plus for risk assets, assuming the decrease in market rates and flattening yield curve aren’t precursors to a recession, a credit event, or an unruly setback catalyzed by the unraveling of a trade deal with China.

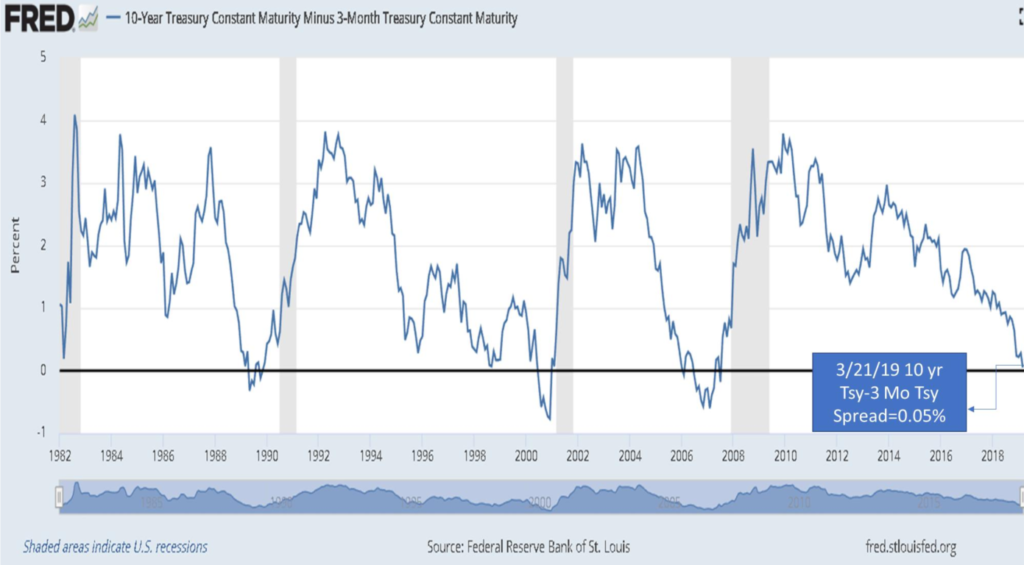

The graph below depicts the 10-year Treasury Yield Minus the 3-month Treasury Yield (“10-Yr – 3-Mo Tsy Spread”) courtesy of the Federal Reserve Economic Data unit out of the St. Louis Federal Reserve Bank. The 10-Yr – 3-Mo Tsy Spread has been a reliable predictor of future recessions which occur between 9 to 18 months after this spread turn negative. Today, the spread is a positive 0.05, tantalizing close to turning negative. In mid-1998 this spread also was tantalizing close to turning negative, but turned out to be a false positive as the economy roared ahead and was only derailed by the implosion of the technology, media and telecommunications bubble in early 2000 which resulted in a mild recession in 2001 as market prices plummeted and the negative wealth effect dampened economic activity. Will the spread turn and stay negative? The stock market is behaving right now as if it is improbable.

The stock market essentially fears no evil now, because it is confident that it has the “central bank put” at its side. However, investors need to be cognizant that the “central bank put” today is not the same as it was in 2009.

In 2009, it was an act of reassurance, controversial though it was. Today, it has the semblance of being an act of desperation.

Desperate times, though, call for desperate measures; and every central banker must be praying this policy palliative is enough to avoid a global recession, because they all know their ability to use interest rates to fight the next recession is diminished.

For now, the stock market is riding a wave of price momentum and trading with a Pavlovian reflex to buy stocks when the Fed, and other central banks, are ringing the bell of easy monetary policy. It has been further supported by performance chasing and efforts to re-risk after the widespread de-risking in the fourth quarter.

Stock market action is all on the up-and-up right now, because nothing has happened yet to upset the view that a second half recovery is going to happen. Accordingly, stock market participants are settling back into old ways, riding the central bank put to strong returns that were there for the taking with the discounted valuation entering the year.

With the S&P up 13.9% already in 2019, though, it should be easy does it for investors just now trying to chase this market. The S&P 500 is apt to take a run at its all-time high, yet valuation isn’t as attractive as it was entering the year, and economic and political risks remain prominent.

Positive price returns have been easy for the market so far in 2019, yet the easy money generated by the Fed pivot to its old ways has probably already been made.

As always, I look forward to hearing your comments and questions.

Warm regards,

John P. Swift, CFA, CPA

CEO & Chief Investment Officer