The Age of Volatility

John P. Swift, CFA, CPA Chief Investment Officer

312-259-9595 or jswift@trustbenchmark.com

September 27, 2020

Taking Advantage of Volatility

Nobody doubts that the next several months could be accented with a good deal of volatility, making it more of a active manager’s market. The volatility could ultimately expose some good long‐term investment opportunities, but patience will continue to be a virtue. Patience is a hallmark characteristic of the investor class; and history has shown that it pays in the end to be patient if time is on your side to stay the course during periods of increased volatility ‐‐ and even large market declines. One thing that can be concluded from stock market history is that the stock market is a wealth‐generating machine for investors able to stand the test of time. Some periods are more challenging than others, and 2020 has been one of those periods and the year is not over yet.

A patient strategy that takes full advantage of volatility is selling cash-secured put options. The other side of that put option trade is to buy a put option which gives you the right, but not the obligation to sell a security at the agreed upon strike price. The buyer of a put option is buying insurance or “hedging” their downside risk. They are

worried about a price decline in stocks that they own and are willing to buy short-term insurance to cover these potential losses by buying a put option.

Conversely, the seller of the put option is the insurance company. As the insurance company, you collect the premium and wait for the stock to fall in price to the point that you are “put” into the stock. If the stock does not fall in price or goes up, you renew the sold put position, collect the premium and wait and see what happens.

Now, in a volatile market option prices get more expensive for the option buyer. Conversely, the seller receives a larger premium for selling the put option. Under volatile market conditions it is common that you can receive premiums on the sold put option equal to 1%-3% of the market price of the underlying stock on a 30-day option contract at strike prices that are priced 10%-15% below the current stock price. Now, getting paid 1%-3% of the stock price every 30 days while you wait for the opportunity to buy into a world class firm at prices 10% to 15% lower than the current price is an attractive opportunity for the patient investor, and it is a great way to profit from the known phenomenon that these put options are routinely overpriced. Insurance in the investment markets is awfully expensive, and it is good to be the insurance company under these circumstances.

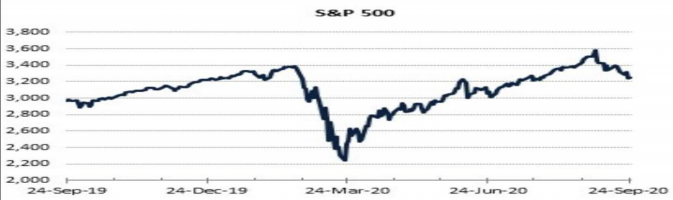

S&P 500 Still in Positive Territory

The fact that the U.S. market is still in positive territory is a testament to its ability to climb a wall or worry. Consider that U.S. equities are still in positive territory in spite of the fact that we are living through the worst pandemic in more than 100 years, experienced the highest unemployment rate since the Great Depression, suffered through the largest ever quarterly decline in real GDP in the second quarter, rolled our eyes at the inability of Congress to pass additional fiscal relief, and are presently stressing out over the potential for a contested presidential election. Through it all, the market endures on the back of the U.S. consumer bolstered by fiscal and monetary relief. How consumers spend money during this pandemic has changed dramatically and there have been and will continue to be winners and losers in this realignment of American and global consumerism.

Stay at Home vs Recovery Stocks

The past several weeks have been filled with headlines about the inability of Congress to agree on additional government stimulus, Supreme Court nominations, and the presidential election. The recent gains on NASDAQ stay-at-home stocks such as PayPal (PYPL) suggests that it was the fear of another COVID-19 wave that has moved the broader market lower while stay-at-home stocks such as PayPal, Microsoft, and Apple rebounded.

Last week began with the UK talking about a second shutdown and ended with all of Europe facing down a second wave of infection as France reported its highest number of daily cases. In the U.S., the number of cases is rising leading to the fear of new shutdowns which sent investors towards safe-haven, stay-at-home stocks over recovery plays. For example, Amazon (AMZN), Apple (APPL), and Microsoft (MSFT) have been up in the face of the recent sell off while recovery plays such as Chevron (CVX) and value stocks are getting clobbered.

We believe in using volatility to our advantage, as discussed above, to use these pullbacks and corrections to add to world class businesses. The economy continues to improve, and the pandemic has motivated firms to rethink their cost structures resulting in improved profitability leverage in the face of an improving economy.

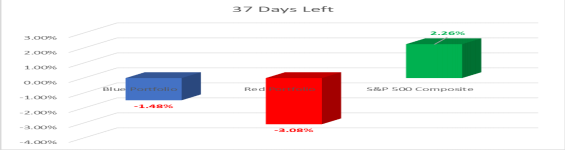

Red vs Blue Portfolio Presidential Election Tracker

The U.S. presidential race entered its final and most crucial stage this week, with Republican President Donald Trump facing his Democratic challenger, former Vice President Joe Biden, in their first and most important debate on Tuesday evening. The world will be watching.

The presidential and congressional elections have been a sideshow for months but are now moving into the Big Tent of this on-going circus. While the voters will be watching the debates, financial and economic variables will have more impact on the presidential outcome. In addition to tracking the “Blue vs Red” portfolios, we have constructed a four-variable model which includes the S&P 500 performance with a starting point 100 days out, the incumbent’s approval rating, the state of the economy, and the value of the U.S. dollar. On the dollar variable, a weaker dollar helps exports and provides an economic tail wind. A weaker dollar generally helps the incumbent in an election year.

Although this model shows the current race tighter than the polls would suggest, a renewed flare up in COVID-19 cases could move the emphasis back to President Trump’s handling of the pandemic and the state of the economy.

Additionally, the Supreme Court nominee, Judge Amy Coney Barrett, will create another sideshow to the circus, but if history is any judge, her nomination might not be a significant factor in the presidential election outcome as either side of the political spectrum may think. First, there have been 29 previous instances where a president was presented with a Supreme Court vacancy during an election year, and in all 29 cases the sitting president fulfilled

their constitutional mandate and made a nomination prior to the election or during the “lame duck” session between the election and the seating of the president-elect.

In 16 of those 29 occurrences the sitting president was up for re-election. In those 16 instances, a small sample size, the president won re-election 13 times or 81.3% of the time. Of the 45 previous presidents only 10 have not won re-election when they elected to run for re-election (President John F Kennedy was assassinated before he could run for re-election) for a winning percentage of 77.8%. Statistically speaking, the small sample size makes

any inferences from these 16 occurrences subject to a material amount of statistical error, but it does provide some evidence that these election year Supreme Court nominations do not materially affect the presidential voting outcome. The impact on the senatorial races is also unclear, but voting trends in the House and Senate tend to follow those affecting the presidential race.

One of the main variables of our four factor presidential model is the performance of the S&P 500 during the 100 days leading up to the election, and on that variable the S&P 500 remains in positive territory, up 2.3%. Both our “Blue and Red Portfolios” are under water since the “100 days out” starting point. I do not know how to read into

that sub-plot other than to surmise that the market has more faith in the U.S. consumer than it does in either candidate, and perhaps on this point we can all find something we can agree on.

Catching Up

We look forward to catching up with each of you, and we will be reaching out to schedule a time to meet over the phone or by a Zoom/MS Teams video link. In the interim, if you would like to get something on the calendar, please send me a note with some dates and times.

Warm regards,

John