The Fed and Inflation

John P. Swift, CFA, CPA Chief Investment Officer

312-259-9595 or jswift@trustbenchmark.com

August 30, 2020

Upcoming COVID Vaccine Phase 3 Test Update

Please mark your calendars for a very impactful update on the status of the Phase 3 COVID vaccine trials that will be held on Wednesday, September 9th at 10 AM CT (11 AM ET). We recently provided an invitation to all the recipients of these market notes, and if you are unable to attend, we will be making available a podcast of the event on our Benchmark website, as well as our LinkedIn site.

The world is about the learn whether any among the first wave of COVID-19 vaccines will work, and the health of everyone in the world depends on one or more of these candidates to succeed. Also, in play is approximately $100 billion in investor money worldwide which reflects the value the stock market is placing on the COVID-19 vaccines. Will we get a peek at the early results? I am as excited as anyone and anticipating a large turnout for this important event.

If you did not receive an invitation, please drop me an email. Additionally, please forward the invitation to other interest parties. We have provided for a large “virtual auditorium” for this event, so space is not limited.

Federal Reserve Speech

The Federal Reserve’s annual Jackson Hole Summit, billed as “Fly Fishing and Finance”, was held virtually from Kansas City this year for reasons all too familiar. I hear the KC Zoo is nice, but they frown on fly fishing within its friendly confines.

Federal Reserve Chairman Jay Powell provided the keynote address where he outlined a paradigm shift with respect to the stated Fed policy of inflation targeting. As you know, the Fed’s former policy was to target inflation rates at 2% while maintaining full employment. The tweak to that policy outlined by the Fed Chairman was that the 2% inflation target will now be an average figure which, when you consider that we fallen short of maintaining the 2% target over the past eight years, means that the Fed will tolerate higher than 2% inflation for some period such that the average inflation over some specified period of time equals 2%.

One of the takeaways is that the Fed will be slower to raise interest rates which would allow unemployment to remain lower for longer. The other important point is that we achieved all-time lows in unemployment for several years prior to the pandemic without inducing higher levels of wage-based inflationary pressures. That adds up to low interest rates for years to come. The futures market does not expect the federal funds to raise above its current range of 0%-0.25% until late 2024.

Many observers have worried about higher inflation reminiscent of the 1970’s. Others have been tormented that this would usher back into style wide lapels, double knit suits, and bell bottoms. But fear not inflation-fearing fashionistas! Back in the 70’s, baby boomers were flooding the job market, we produced what we consumed here in the U.S., and the labor unions held sway which provided for the wage-price spiral. Today we have slow labor force growth, and higher cost labor many times either gets replaced with cheaper workers abroad or cheaper technology. The job growth that we have experienced is in the lower wage services sectors such as retail, hospitality, and leisure. Add this all up and you can better understand why we are rewriting the books on inflation and full employment.

Another reason to move to inflation averaging is a bit more arcane, but it deals with inflation expectations and its potentially deflationary affect on interest rates. The yield on a risk-free bond (U.S. Treasury bonds, for example) are a combination of some small real yield plus the market’s forecast for average inflation over the life of the risk-free bond. As that inflation expectation gets lower, so does the nominal yield on the risk-free bond and interest rates, generally. Lower interest rates take away from the Fed’s ability to lower them in the event of, say, a pandemic or lower than desired employment rate and economic output. Today, the 10-year breakeven inflation rate that would make investment in a 10-year Treasury bond equivalent to putting your hard-earned money into a 10-year Treasury Inflation-Protected security is only 1.65%. In other words, the market presently does not expect the Fed to be able to maintain a 2% inflation rate for more than the next two U.S. Presidential terms. This lower inflation expectation steals dry powder from the Fed from one of their most effective policy tools, the Federal Funds Rate.

The main beneficiaries of this average inflation rate policy are borrowers and investors. The Fed needs lower rates to help finance the massive federal deficits while investors benefit by higher valuations due to lower than expected discount rates applied to future cash flows which increases their present value.

Within the investment markets mega-cap growth stocks within the technology sector have soared which has resulted in some rather astonishing and, in some cases, overstretched valuations. Prospectively, in a COVID vaccine world, value and cyclical sectors will finally have their day in the sunshine given their economic sensitivity, as well as historically low valuations relative to their growth peers. Finally, one potential problem for all equities is that this new inflation policy could trigger more speculation and risk in finance at a time where valuations are already stretched.

A Fixed Income Alternative in a Zero-Bound Interest Rate World

With the 10-year Treasury Bond yielding a paltry 0.70% and the Federal Reserve pursuing rates beyond 2%, the risk of eroding your purchasing power of your bond principal is pushing fixed income investors to consider other markets such as real estate and commodities such as gold.

We have another idea, Limited Risk Equities.

We define Limited Risk Equities as firms that have a much higher dividend yield on their common stock versus their yield on their senior corporate debt tranche. We also eliminate equities that do not maintain a free cash flow/dividend ratio of at least 3.0 and payout more than 85% of their annual cash flow earnings in the form of dividends. Finally, we screened out equities with less than a 1% spread between their dividend yield and their senior bond yield. Accordingly, what follows are eight Limited Risk Equities which we believe should be considered as a replacement for, at least, a small sleeve of investor’s current fixed income exposure.

| Company/Ticker | Stock Yield | 10-Year Bond Yield |

| Edison Intl (ED) | 5.0% | 2.0% |

| Johnson & Johnson (JNJ) | 2.7% | 1.0% |

| Kellogg (K) | 3.3% | 1.6% |

| Merck (MRK) | 2.9% | 1.2% |

| Pepsi (PEP) | 3.0% | 1.2% |

| Pfizer (PFE) | 3.9% | 1.3% |

| Proctor & Gamble (PG) | 2.3% | 1.2% |

| Verizon | 4.2% | 1.6% |

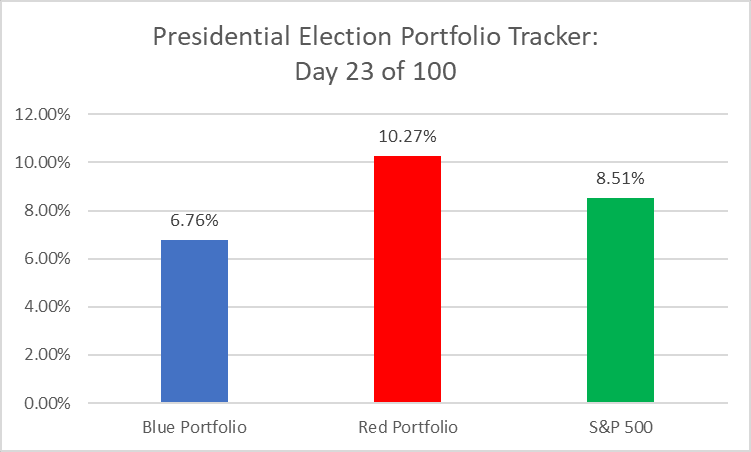

Blue vs Red Presidential Election Portfolio Tracker: A Post Convention Update

A valid criticism of our “Blue vs Red Presidential Election Portfolio Tracker” was raised this week (by me) in that their have only been 20 presidential election cycles in the modern times, and 20 data points can not provide for a statistically significant result. While that is true statistically, the evidence over these 20 “trials” has indicated that these market-based approaches towards handicapping the outcome will become very statically relevant.

Against that backdrop, what follows is the current Blue vs Red portfolio status. I have mentioned this before, but it bears repeating that we started tracking these portfolios when we crossed the “100 days until election” date several weeks ago, but the real action will not start happening until after Labor Day. I am particularly interested to see how these portfolios react in the aftermath of the first presidential debate. I would also be interested in seeing how these portfolios react if the former VP declines the invitation to debate. Joe Biden has consistently indicated that he will debate President Trump, but there’s a rising chorus within the Democratic Party that are urging him towards not participating led by House Speaker Nancy Pelosi.

We will save for another day the results to whatever path is chosen on the debates, and what follows are a first look at the post RNC and DNC conventions.

The surge in the Red portfolio appears to be in step with the recent polling figures which have seen President Trump moving much closer to former Vice President Joe Biden especially in the “swing states” Pennsylvania, Florida, Michigan, Wisconsin and Arizona that will most likely determine the election.

Again, it is early. Stay tuned.

Catching Up

We look forward to catching up with each of you, and we will be reaching out to schedule a time to meet over the phone or by a Zoom/MS Teams video link. In the interim, if you would like to get something on the calendar, please send me a note with some dates and times.