The Way Forward: Separating the Winners & Losers

John P. Swift, CFA, CPA Chief Investment Officer

312-259-9595 or jswift@trustbenchmark.com

May 04, 2020 – Webinar and Presentation

We did this presentation on Tuesday, view PDF or watch the video.

The Way Forward for the Stock Market

The S&P 500 saw a 35% decline from its February 19th high and matched it with a 35% gain off its March 23 low, since then. That does not mean we are back to where we started. The math does not work that way. To get back to where things stood on February 19th, the S&P 500 would have to climb 55% from its March 23 low. But let us not allow a bit of depressing math dampened our spirits, it has been a remarkable move off the bottom if one wants to call it “the” bottom.

S&P 500 Price Return-February 19-May 1, 2020

So, as we move into May with over $2 trillion of fiscal stimulus approved, clearance for the Federal Reserve to provide upwards of $4.5 trillion of credit support, and indications that remdesivir, a COVID-19 treatment from Gilead Sciences (GILD), has been effective in treating hospitalized patients with severe cases, the question must be asked:

What does the way forward look like?

Challenges Ahead

Here are some things we know (and the market knows) as we contemplate the near future:

- Second quarter GDP and earnings are going to be awful.

- There have been 30.3 million officially reported jobless claims over the last six weeks. There will be more to come, and that level of unemployment is going to be a major drag on consumer spending.

- States will be increasingly reopening their economies and better economic activity will be seen.

- Banks, while doing what they can to provide financial support/relief, will nonetheless be tightening their lending standards.

- Share buyback activity is going to be curtailed significantly, except for Big Tech companies that we will discuss later in this note.

- Capital expenditures will be greatly reduced given the uncertain demand outlook.

- The bipartisan spirit of compromise in Washington over fiscal relief will turn partisan again as the November election draws closer.

- There will be quite a bit of rehiring activity, but the unemployment rate is going to remain remarkably high since many businesses won’t be reopening at the same level, nor will they see the same level of customer activity as they did before the shutdown.

- The geopolitical environment will get more contentious due to the socio-economic dislocations caused by government responses to COVID-19, efforts to seek reparations of some kind from China for its handling of the coronavirus pandemic, and strained budgets.

- 2021 will remain the benchmark for earnings prospects.

- The Fed will remain a support mechanism for the stock market.

This list is not comprehensive, but It offers an awareness that, while the worst of the COVID-19 shutdown impact is presumably behind us, the road ahead will continue to have its challenges.

That will be true for the economy and it should be true for the stock market, which has priced in a lot of potentially good news with the prospect of recovery, reopening and remdesivir.

A Gut Check Coming

When the stock market closed on April 30, it was trading at 20.5x forward twelve-month earnings. That is a 37% premium to the 10-year historical average, according to FactSet.

Source: Facset

That seems rich, to say the least, given what is going on around us and given that the recovery from what is going on around us is not going to be easy.

Of course, we keep hearing that valuation does not matter right now. What matters reportedly is the Fed’s liquidity backstop and the progress toward finding a vaccine for COVID-19, the introduction of which is seen as the silver bullet.

A COVID-19 vaccine would indeed be the best news for what ails the world, and because it was said in March that a vaccine was likely 12-18 months away, the stock market has managed to trade with the optimism toward a vaccine arriving sometime in 2021 (if all goes according to scientific plan).

It is all part of the bridge-building effort to a better tomorrow. The Federal Reserve is the foreman of that build while the scientists are the workers. The stock market has been banking on their success, but with any large construction project, there are bound to be setbacks, delays, and change orders.

This should create some stumbling blocks for the highly valued stock market as the economic reality on the ground diverts the nearly undivided attention the market showed in April to building a bridge to the other side of this pandemic.

Call it a gut check that should keep the market in check in the absence of a vaccine.

What this Means to Investors

The economic picture is not nearly as good as the stock market has made it out to be, nor will it be soon. But that is the thing with art: beauty is in the eye of the beholder, and the stock market has been enraptured by the Fed’s liquidity brushstrokes that have painted over credit market issues.

But, now, we enter a phase where the hard part of the recovery begins — when the speculative hope clashes with the fundamental reality on the ground. Accordingly, risk-reward dynamics will be reassessed and likely challenged with more resistance than has been seen in the move from 2191 to 2954.

May has started on a rocky note, and the budding talk that the U.S. is considering retaliatory measures against China for its handling of the coronavirus pandemic is creating a new layer of angst for investors at a time when more angst isn’t needed.

It is a reminder that the easy part of the recovery rally in the stock market is over. That is not to say we could not see more upside, but at 20.5x forward twelve-month earnings, the near-term upside potential looks limited in the absence of a vaccine while the downside risk has increased.

Separating the Winners & Losers: Consumer Spending is Key

Yet another economic indicator is now the worst on record: On Thursday, the Commerce Department reported that consumer spending dropped 7.5% in March, the biggest one-month drop since the government began tracking in 1959. While economic indicators across the board are problematic, the consumer spending figures loom large—the global economy simply cannot recover without the consumer.

The $22 trillion U.S. economy rests on consumer spending which accounts for 70% of total economic output. How, where, and when people choose to spend their money from here on out will shape companies’ reopening plans—and serve as a harbinger for the broader economic recovery.

Past recessions have typically started elsewhere—like in energy or banking—and then bled into the consumer as job losses piled up. But consumers are on the front lines of this downturn, and the sectors dependent on their spending—travel, leisure, retail, restaurants—have been among the most battered as governments pause their economies to contain the pandemic.

Reopening will not be easy; governments and companies must walk a fine line between reopening and avoiding another wave of Covid-19 outbreak. Some companies, such as Starbucks (ticker: SBUX) and Macy’s (M), already have plans to reopen stores beginning next week. But it is far from business as usual in terms of operations, and retailers will also likely find a much-changed consumer, a byproduct of strained budgets and trepidation about the future.

Unemployment & Consumer Spending

Some 30 million Americans have lost their jobs in six weeks, dealing a sizable blow to household budgets. The jobs most immediately at risk are in the areas you would expect—accommodation, food services, retail, construction, and manufacturing—but the fallout could be much broader. More than a quarter of 100 large U.S. companies disclosed furloughs or voluntary leave at low to no pay as of April 21—quadruple the number on March 24. White-collar workers, including those who can work from home, are among those seeing paychecks cut or deferred—an unusual phenomenon that suggests the crisis could hit the spending of various income groups.

Unfortunately, Americans have little buffer: More than half of U.S. households do not have any emergency savings to tap in a crisis. Even a quarter of households earning more than $150,000 lack one.

Credit card balances were already climbing ahead of the pandemic, hitting $1.1 trillion in February; the ratio of debt to net worth in the middle class was higher than for other groups. And now Americans are missing payments, with several credit companies bracing for fallout. American Express (AXP), for example, has tripled its credit loss provisions.

There is also a psychological impact. As stores and restaurants reopen, consumers’ experience with the coronavirus will affect their risk tolerance for venturing out. Those older than 65 represent roughly a fifth of total consumer spending and may be among the slowest to go out again as they are among the most vulnerable to the virus.

What Will Consumers Spend Money On?

No one has the urge to spend less on their own because they will feel deprived. However, when everyone spends less, you do not feel deprived which offers an opportunity for Americans to reassess their spending.

That consumer behavior has already proven true: For the week ending April 12, credit card spending was down 34.4% and debit card spending was down 14.6% in the states hardest hit by the pandemic, including California, New York, New Jersey, Illinois, and Louisiana. But spending in the eight states without “stay at home” orders was not much healthier, with credit card spending down 29.5% and debit card spending down 11.7%. Only a fifth of Americans surveyed by Gallup said they would resume normal daily activities “immediately”; 70% said they would “wait to see what happens with the spread of the virus before resuming” and the rest said they’d limit social contact “indefinitely.”

Empty Shops

Traffic to retailers plummeted in mid-March as states implemented stay-at-home orders. The question now: Will shoppers return as restrictions are eased?

Consumers surveyed in France, Germany, Italy, Spain, the U.K., and the U.S. were spending 25% to 30% less than before the virus as of April 21, according to Deutsche Bank. European retail chains have warehouses full of collections that are now out of season and fashion, and the cost of storing it all for another year exceeds their low profit margins. German consumers surveyed in mid-April found that less than a quarter were optimistic about an economic recovery.

Once the health crisis moderates, respondents said they plan to curtail some in-person activities and reduce their online grocery purchases. Staying in could cause broader pain: Eating out accounts for 60% to 80% of all food service revenues, according to a March report by Rabobank.

China’s Reopening Experience

China has reopened much of its economy, but consumer spending and retail sales are still depressed—even after China sent vouchers to households to entice them to go out and spend. Another survey of Chinese consumers found 30% used less skin care and bought less alcohol, and more than half used less makeup. But among wealthier respondents in China’s bigger cities, 30% bought more skin care than prior to the crisis—an indication of the trend toward health and wellness that many analysts expect will accelerate in the U.S. as well. Baby boomers may be more careful in how they re-engage with society, which could lead to less spending on travel and more on their homes or health and fitness.

A reluctance to go out until there is a vaccine or treatment will hurt the sustainability of consumer-oriented companies and their labor force. In the U.S. half of consumer spending could be at risk. Once the economy stabilizes in 12 to 18 months, consumer spending will likely be a smaller slice of the economy by a couple of percentage points.

Americans, however, do love to spend, and we are optimists by nature. We found a ray of light in the Conference Board’s index of consumer confidence, which fell to its lowest reading since mid-2014. We noted that the most surprising part of the report was an increase in consumers’ expectations for six months in the future, hinting at a pent-up desire to spend.

But pent-up demand—an invocation used to will a speedy economic recovery—is not enough. No matter how many people are eager to return to their spendthrift ways (or how many can still afford to), companies are going to have to adjust how they cater to consumers. And for many, those adjustments will come at a cost.

Getting customers in the door could require profit-eroding changes—such as flying less-full airplanes and reducing seating capacity in restaurants and theaters. Further complicating the situation: This is when retailers order for the crucial back-to-school and holiday shopping seasons, an already-challenging exercise in predicting demand that is further complicated this year by uncertainty about supply and the mix of school spending if more students and educators opt for online educational delivery.

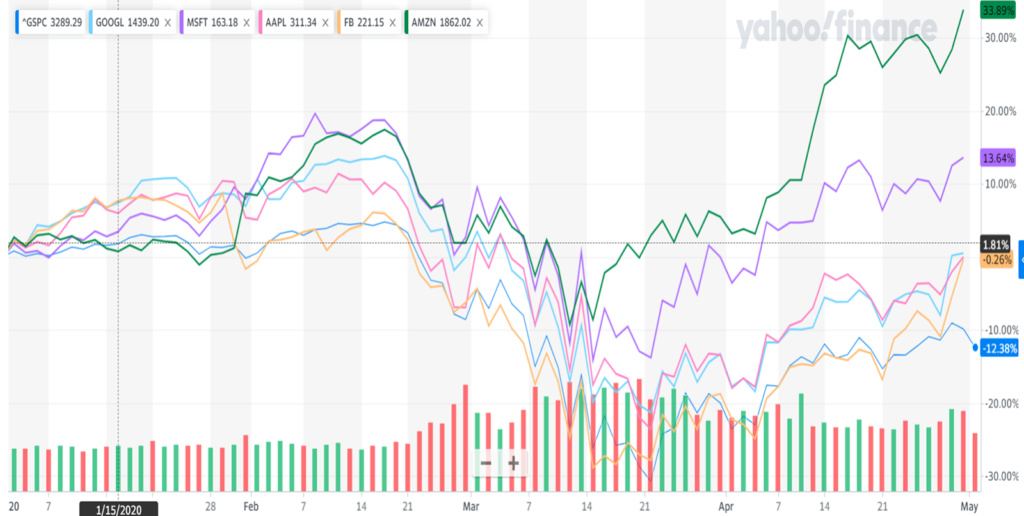

Separating Winners & Losers – The Big Winner – Big Tech

In just three days over the past week, our five largest positions, Microsoft (MFST), Amazon.com (AMZN) Apple (AAPL), Alphabet (GOOGL), and Facebook (FB) – all reported earnings. They also happen to be the five largest companies in the S&P 500, so the results mattered—a lot, to both us and the market. The news was better than feared, though plenty of questions remain.

What bear market?

While the S&P 500 was still down 11% year to date through Thursday’s close, the tech-heavy Nasdaq Composite is basically back to flat. Most of the credit goes to these tech giants. In April, the S&P 500 rallied 12%, and big tech still managed to outperform, led by gains of 23% for Facebook (ticker: FB) and 27% for Amazon (AMZN). All five of these companies will exit the crisis stronger than they began. They have sterling balance sheets, dominant market positions, and smart management. The crisis is only accelerating their lead.

Apple has 550 million subscribers to various services. Microsoft’s Azure cloud is growing revenue at nearly 60% a year. In just a few weeks, Amazon hired 175,000 people. And Facebook just hit 3 billion users—nearly 40% of the earth’s population. The big tech names are getting bigger.

Better than advertised.

Digital advertising was one of the primary worries for the internet sector heading into earnings season. Airlines, hotels, retailers, restaurants, and movie studios—all large online ad buyers—have little reason to promote themselves, while small businesses are focused on conserving cash. The quarter’s biggest surprise was that Google’s parent Alphabet and Facebook both said that advertising demand had stabilized in April.

Weakness in sectors such as travel and small business were offset by strength in direct-to-consumer retail brands, technology, and gaming. Both Facebook and Alphabet warned that risks remain, that the June quarter would be tougher, and that extrapolating from April is risky. But, for now, online advertising is proving more resilient than expected.

“Big Tech” vs S&P 500 – YTD as of May 1, 2020

Backing Buybacks.

Much of the corporate world has suspended buyback programs. But not big tech.

Alphabet bought back $8.5 billion of stock in the quarter, a record quarterly haul; Microsoft repurchased $6 billion, and Apple bought back $18.6 billion, while raising its dividend 6%. Apple also announced a $50 billion buyback program, on top of its existing $40 billion authorization. Investors want repurchases, and we defend the companies’ right to make them. They are still hiring people, they spend freely on research and development, they have ample cash, and they continue to generate lots more. Most importantly, none of them is taking government stimulus dollars. Why shouldn’t they buy back shares?

In Search of Guidance.

It is good news that big tech did better than expected in the March quarter. But let us remember that it was mid-March or later before the shutdowns really started. The economic pain did not hit full force until the current quarter. Amazon says it could be breakeven or worse in the June quarter, as the company ramps up Covid-19 related spending. Apple says that iPhone sales will be materially worse. The ad recoveries at Facebook and Alphabet are nice, but year-over-year comparisons in June are going to look worse than March’s. Microsoft’s cloud business looks strong, but the company will not be insulated from a deep recession. No one will be. So, it is fine to breathe a sigh of relief over the first quarter. But keep your mask on; we are not done yet.

Consumer Spending – Scenario Based Winners & Losers

Investors have some options, depending on their level of optimism. We have looked at how companies would fare in three scenarios.

Scenario # 1 – Mostly Successful Economic Re-Opening with Social Distancing – Most Likely

Under our most likely scenario where stores reopen but must abide by strong social distancing rules, we expect a divergence in performance. Sales for companies with the least impact from such guidelines will rebound the strongest; staples like Procter & Gamble (PG), Mondelez International (MDLZ), and Kimberly-Clark (KMB), for instance, and companies that offer an easier one-stop, in-and-out experience are also well-positioned. The list of relative winners in this scenario include Lululemon Athletica (LULU), Estée Lauder (EL), Autozone (AZO), fast-food chains like Domino’s Pizza (DPZ), Wendy’s (WEN), and Jack in the Box (JACK), and discount retailers like Dollar General (DG).

Scenario #2 – Sustained Closure from COVID Relapse – Somewhat Likely

If there is a sustained closure of retail and restaurants through the summer and into the end of the year, possibly due to a second wave of infections, we expect consumer staples stocks and “essential” retailers with open stores to outperform, as well as discretionary companies that have good liquidity and can grow their online sales. That includes Walmart (WMT), Nike (NKE), Target (TGT), and Dollar General (DG). Relative losers in this scenario would include mall-based retailers with liquidity challenges, such as Macy’s (M), Gap (GPS), Signet Jewelers (SIG), and Nordstrom (JWN), and any store without much of an online presence.

Scenario # 3 – Mostly Successful Re-Opening with Deep, Enduring Recession – Least Likely

And if stores reopen, but there is a deep recession, we looked for companies that fared relatively well during the 2008-09 downturn and that could also benefit from consumers getting stimulus payments.

That includes fast-food chains like McDonald’s (MCD) ; auto parts companies like AutoZone (AZO) and Advance Auto Parts (AAP); dollar stores like Dollar General (DG) and Big Lots (BIG), as well as the likes of Walmart (WM) and J.M. Smucker (SJM).

Upcoming Webinar

We are hosting a webinar on Tuesday, May 5th entitled “The Way Forward: Separating the Winners & Losers” at 3 PM CT (4 PM ET) which will offer a Q&A session at the end of the program. If you have not done so already, you can Register Here.

Catching Up

We look forward to catching up with each of you, and we will be reaching out to schedule a time to meet over the phone or by a Zoom video link. In the interim, if you would like to get something on the calendar, please send me a note with some dates and times. I would be delighted to hear from you.

Warm regards, John